I am filled today, as is often enough the case these days, with a sense of righteous indignation. In a meeting earlier today, Dominic Cull (firebrand lawyer for the forces of telecommunications good in South Africa) pointed out the obvious. He said that one of the single most important things mobile operators could do to make a difference for the poor would be to drop the price of SMS charges. The funny thing about the obvious is that we often don’t see what is staring us in the face.

For those who may not be familiar with the technology of SMS, it doesn’t cost a mobile operator very much to send and receive SMSes. In fact, for GSM networks, SMSes are sent on a signalling channel which means that they don’t actually take up any traffic that would otherwise be used by voice calls. So, with voice infrastructure, mobile operators basically get SMS infrastructure for free. Now, that doesn’t mean that it is free for operators to provide. There are obviously billing and technical systems that need to be maintained to ensure that SMSes continue to function but it is about as close to free money as you can get.

For those who may not be familiar with the technology of SMS, it doesn’t cost a mobile operator very much to send and receive SMSes. In fact, for GSM networks, SMSes are sent on a signalling channel which means that they don’t actually take up any traffic that would otherwise be used by voice calls. So, with voice infrastructure, mobile operators basically get SMS infrastructure for free. Now, that doesn’t mean that it is free for operators to provide. There are obviously billing and technical systems that need to be maintained to ensure that SMSes continue to function but it is about as close to free money as you can get.

About a year ago there was a blog post on the high cost SMS, subsequently picked up by Slashdot, which raised a small storm of indignation about the cost of SMS. In December last year, New York Times published an article highlighting the failure of the chair of the Senate anti-trust subcommittee to get anything like a reasonable explanation from operators on why SMS charges in the U.S. had doubled between 2005 and 2008 in the United States.

So what are the facts? The global average cost of an SMS is about 10 U.S. cents per message. Here in South Africa the cost of an SMS is R 0.75 or about 7 U.S. cents per message. Doesn’t sound like very much until you consider that, according to the ITU in 2006, the global SMS market is worth about 80 billion U.S. dollars annually. The New York Times article estimated that 2.5 trillion SMS messages were sent globally last year. A Huawei article estimates that 80-90% of SMS revenue is profit.

How is this possible? Why haven’t market forces brought the cost of an SMS down to something somewhat related to its cost + a reasonable profit? Why are consumers paying ten times the cost per SMS? Communication technology has gotten more sophisticated, less expensive, more automated and SMS volumes have sky-rocketed, yet on average cost per SMS has gone up. So what is up with that? A communications regulator doesn’t have to look much further for evidence of market failure.

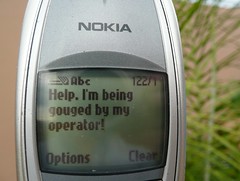

So why do people put up with this? Partly, I think it is because behaviour in spending on mobiles is not entirely rational. Having anchored high prices for SMSes, it is comparatively easy for mobile operators to simply carry on charging high prices. Everyone, rich or poor, needs access to communication. For the poor, as expensive (comparative to cost) as SMSes are, they are still the cheapest form of pervasive electronic communication. Consider this in a context where poor Africans are spending over 50% of their disposable income on mobile communication (see the table below for more detailed information). What this amounts to is a level of price gouging on the part of mobile operators in developing countries that verges on the criminal. They make the highest profit margin on the service the poor need most.

So here is my proposal. The 1 cent SMS. Let’s challenge mobile operators to make a real difference to the poor by dropping pay-as-you-go SMS charges to 1 U.S. cent per message. Applied globally that would reduce SMS revenue to 8 billion dollars; arguably still a tidy sum. However, that is not taking into account the upside for operators. The reduced SMS costs would enable increased SMS traffic and new, as yet unthought of SMS-based enterprises such as Nathan Eagle’s innovative txteagle start-up.

To get a more complete sense of what people are paying for mobile communications in Africa, here is an excerpt from Alison Gillwald and Christoph Stork’s 2008 publication “Towards Evidence-Based Policy: ICT Access and Usage in Africa“, published by Research ICT Africa,

Monthly expenditure for mobile telephony as share of income and disposable income

| Monthly mobile expenditure / monthly individual income | Monthly mobile expenditure in / monthly disposable income | |||||

| All | Bottom 75% in terms of individual Income | Top 25% in terms of individual income | All | Bottom 75% in terms of disposable Income | Top 25% in terms of disposable income | |

|

Benin

|

11.7%

|

18.0%

|

7.9%

|

32.9%

|

39.8%

|

28.0%

|

|

Botswana

|

10.4%

|

14.9%

|

6.1%

|

43.2%

|

50.4%

|

30.6%

|

|

Burkina Faso

|

14.1%

|

19.3%

|

7.6%

|

32.3%

|

42.1%

|

22.6%

|

|

Cameroon

|

10.8%

|

16.0%

|

4.8%

|

40.9%

|

47.0%

|

32.8%

|

|

Côte D’Ivoire

|

10.1%

|

14.1%

|

4.9%

|

39.6%

|

47.2%

|

31.3%

|

|

Ethiopia

|

7.1%

|

23.3%

|

6.1%

|

37.0%

|

67.1%

|

35.7%

|

|

Ghana

|

13.0%

|

16.0%

|

7.1%

|

47.9%

|

55.3%

|

34.3%

|

|

Kenya

|

16.7%

|

26.6%

|

7.8%

|

52.5%

|

63.6%

|

39.9%

|

|

Mozambique

|

11.7%

|

17.9%

|

9.2%

|

32.6%

|

50.8%

|

18.3%

|

|

Namibia

|

9.2%

|

13.1%

|

5.7%

|

25.3%

|

32.9%

|

17.8%

|

|

Nigeria

|

13.7%

|

17.0%

|

8.2%

|

52.4%

|

60.9%

|

28.9%

|

|

Rwanda

|

10.3%

|

16.9%

|

8.5%

|

65.5%

|

64.9%

|

65.6%

|

|

Senegal

|

14.2%

|

19.4%

|

9.6%

|

22.2%

|

30.1%

|

13.7%

|

|

South Africa

|

7.4%

|

10.9%

|

4.8%

|

29.3%

|

38.2%

|

16.7%

|

|

Tanzania

|

15.4%

|

22.1%

|

11.5%

|

28.9%

|

40.6%

|

20.5%

|

|

Uganda

|

10.8%

|

18.0%

|

7.4%

|

48.6%

|

68.9%

|

39.0%

|

|

Zambia*

|

10.8%

|

14.4%

|

8.6%

|

60.3%

|

73.9%

|

44.1%

|

* Results for Zambia and Nigeria are extrapolations to national level but not nationally representative.

Good point, Steve. It’s total rubbish that mobile users are being fleeced, especially the poor. Perhaps we should start a campaign for the 1c SMS, on Facebook or Avaaz.org?

Pingback: ICASA - Stealing from AIDS Orphans at Many Possibilities

100% agree to that.

Here in Germany, revenue from SMS was for a long time used to cover up expenses on UMTS/3G licences (which were auctioned by the State some years ago).

Another interesting option could be a flatrate on SMS.

Steve, you’ve nailed it. The question is, how do you create a movement that forces change to happen here?

I think, to be fair, rather consider the following perspective: Granted, there’s an insanely high margin on SMS prices, but just because there’s a high profit margin doesn’t necessarily equate to “we’re being fleeced”.

By and large, SMSes are still pretty cheap, especially if you don’t have access to an application like MXIT, or an MMS-enabled phone (which most of the world now has, probably).

If you SMS frequently enough for it to become a heavy financial burden, you should probably look into cheaper alternatives anyway.

@wogan I think we are talking about different things. I am talking about the more than 1 billion people in the world who earn a dollar or two dollars a day, who are probably still not on a GPRS network, who, even if they did, don’t have a MxIT or MMS enabled phone and for whom SMSes are the cheapest but still expensive for them form of communication.

Don’t get me wrong. I think MxIT is amazing and I think data-based IP phone networks are the future but existing services like SMS will be here for some time to come and they are most useful to those who can least afford them.

@hash Thinking about that. In South Africa, recently the flour milling industry got hit with a R50 million fine for collusion and price fixing. Am wondering if there is not a competition complaint or even a court case. Open to suggestion.

Pingback: Ellipsis Regulatory Solutions... » A Modest Proposal - The 1 cent SMS

High time Steve… you have my full support, and I have no doubt that the APC network worldwide will support this.

Agreed Steve, although (as I am just now telling you on chat!), I think the onus should be on cheaper SMS for pre-paid, which, obviously, is the principal means the poor access mobiles. I’d also add another potential area: most poor people stay in touch the beeping or flashing, as we know, yet tey can only do that if their subscriptions stay active. Most operators shut down pre-paid subscriptions if you haven’t topped up in a certain while. Why not ask that operators make subscriptions available for life, or at least for extended periods (5 years say…one problem with maintaining them for life, is that operators like to pick up old lines and numbers for new customers, which is fair, when network resources are limited).

Pingback: Nathan and the Mobile Operators at Many Possibilities

I totally agree with you Steve. SMS (and USSD) applications will still be around there for a while since it is the basic technology working almost everywhere where GSM network coverage is available, running on almost every phone (compared with the highly fragmented market of OS and platform dependend native phone applications) and it is easy to use – people are used to this technology. With the fact that currently several undersee cables are under construction there will be a change in international bandwidth available in Africa. Maybe not already in 2010 but it will be there within the coming years. Do you think the increased availability of bandwidth will let the telecom operators lower the prices drastically and maybe offer a “GPRS/EDGE/UMTS flat rate”? If so, this would open the door for web based mobile applications.

SMS’s are ripping a excessively large hole out of our pockets, but they aren’t just 140 bytes. On apps like mxit you have connection and transfers happening as well. SMS also has a type of guarantee for delivery and delivery reports.

Most apps I’ve seen must be connected for the message to go through. So if you don’t have access to the network at that time, sorry, you’ve missed your message. They’re also hellishly confusing for some less tech-savvy people to set up and use.

Then there’s the capable phone problem. If your phone is lost, stolen or damaged, you pay a big chunk of money to replace it. If it’s a “fancy” phone, there’s more incentive to steal it, especially in poorer areas.

In some markets, dropping the price as suggested may actually turn out to be a winner not just for the users of SMS’s but also for the operators, who by so-dropping prices will just arouse the interest of a much larger market for SMS’s from among those who hitherto had not afforded them. It may turn out to be a better value proposition for such operators as they make more money at a lower price from disproportionately higher volumes of business!

@Cleophas I couldn’t agree more. See this back of napkin calculation I did comparing South Africa with the Philippines where SMSes really do cost less than 1 US cent.

Pingback: Africa’s Poor: Premium SMS in the Crossfire | WhiteAfrican

Pingback: Tear down that (mobile garden) wall « Crossing the Streams

Pingback: Mobile Operators and Blue Gum Trees «Many Possibilities

Pingback: SMS Interconnect Fees «Many Possibilities

Pingback: How the US can encourage mobile application development « Parallax World

Somali operators offer below 1 cent SMS.

I recently returned from a short stay in Somalia. Here two telecom providers are struggling for market shares. The cheapest and most favored provider Golis Telecom offers users 167 SMS on 1 US dollar, or 0,6 cent per SMS. This clearly shows that your call for affordable SMS services should be possible – if you can make it in a failed state, you should be able to make it anywhere. The big diaspora and remittance industry is another driver in the boost of the Somali telecom sector. Providers offer prices down to 10 cents per minutes for calls to the US. Though coverage outside main cities might be scarce the cell providers are keeping expanding their operation.

What other African countries can compete with such price levels?

Thanks,

Anders

Thanks Anders. That is great evidence. Indeed no one else on the continent can compete with those prices. Perhaps this says that regulators, as currently constituted, are doing more harm than good. Certainly policy complexity appears to be the enemy of competition. Mobile operators seize on policy complexity to deny, debate, delay, and very,very occasionally deliver.

Pingback: How to set up an SMS campaign system | Socialbrite

Pingback: The Importance of Being Local «Many Possibilities

Pingback: 27 months » Blog Archive » Twitter-MTN Partnership & Innovation in Cameroon

Pingback: Safaricom – A Modest Proposal «Many Possibilities

Pingback: Fair Mobile – Two Years On « Many Possibilities